Categories

BUYING, INVESTINGPublished December 27, 2025

Point of Sale Violations Found During Your Home Inspection? Here's What Happens Next (And Who Pays)

Point of Sale Violations Found During Your Home Inspection? Here's What Happens Next (And Who Pays)

You thought the hardest part was over when your home inspection came back clean. But then you received that dreaded call about point of sale violations discovered during the mandatory municipal inspection. Now you're wondering who's responsible, what it costs, and whether your closing date just got pushed back indefinitely.

The reality is that point of sale violations are fundamentally different from typical home inspection issues: and the rules about who pays and what happens next might surprise you.

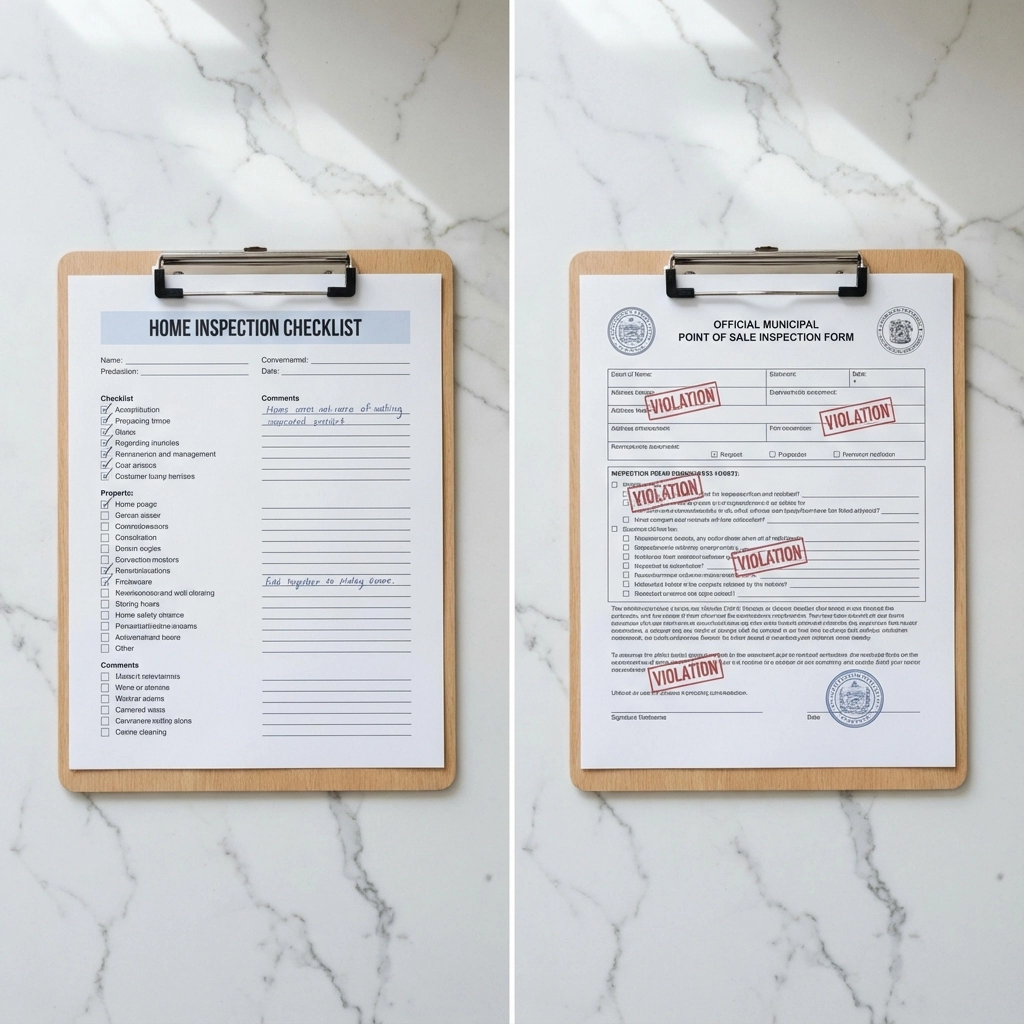

Point of Sale Inspections vs. Regular Home Inspections: What's the Difference?

While your general home inspection focuses on the property's overall condition and safety, point of sale inspections are municipal requirements that verify compliance with local housing codes. These inspections happen at the city level and are mandatory in many Northeast Ohio communities, including Cleveland, Shaker Heights, and Maple Heights.

Here's what makes them different: Your home inspector works for you and provides recommendations. The municipal point of sale inspector works for the city and identifies code violations that must be fixed before the property can legally change hands.

Think of it this way: your regular inspection might flag a loose handrail as something to watch. A point of sale inspection will cite that same handrail as a violation requiring immediate correction before you can close on the sale.

Also note: municipalities handle POS differently. Some conduct exterior-only inspections (sidewalks, driveway aprons, steps, handrails, peeling paint), while others inspect both interior and exterior spaces. Some areas also require add-ons like a sewer dye test or separate exterior sidewalk/driveway compliance. Requirements change—always confirm the current checklist and fees with your city before you schedule.

Who Pays When Point of Sale Violations Are Found?

The short answer: the seller is typically responsible for both the cost of repairs and ensuring violations are corrected before closing. This responsibility exists regardless of whether the sale is "as-is" or includes repair contingencies.

Unlike negotiable items from a general home inspection, point of sale violations aren't optional fixes. The city requires compliance, and sellers cannot legally transfer ownership until violations are resolved or funds are placed in escrow for completion.

When the buyer assumes the POS process (if permitted by the municipality and agreed to in the purchase agreement), the mechanics change:

- Scheduling: the buyer typically schedules re-inspections and coordinates permitted work after the initial city report is issued. Some cities require a signed authorization from the seller before they will speak with the buyer about violations.

- Payment: the purchase contract should state who pays the original POS fee, repair costs, and re-inspection fees. Common structures include a seller credit at closing, a seller-funded escrow, or buyer-paid repairs with a price reduction.

- Responsibility before closing: in many cities, the seller remains the legally responsible party until title transfers or an approved escrow is posted. Even if the buyer is “handling,” compliance still has to meet city rules.

- Re-inspections and approvals: the buyer (or their contractor) arranges re-inspections; however, access and utilities often remain the seller’s obligation until closing.

- Lender impact: some lenders will not allow buyers to assume life-safety violations without a funded escrow. Confirm lender requirements early to avoid delays.

Always confirm your city’s policy—some municipalities do not allow buyer-assumed POS compliance, while others allow it only with specific forms and escrow in place.

What Happens Immediately After Violations Are Discovered

When the municipal inspector identifies violations, you'll receive an official report detailing each issue across potentially dozens of categories. These might include:

- Electrical code violations (outlets, wiring, panels)

- Plumbing issues (fixtures, water pressure, drainage)

- Structural concerns (stairs, railings, foundations)

- Exterior maintenance (gutters, siding, windows)

- Safety equipment (smoke detectors, carbon monoxide detectors)

- Basement and crawl space conditions

The city will issue you a temporary occupancy permit with a specific timeline for completion: typically 30 to 90 days depending on your jurisdiction. In Maple Heights, for example, sellers receive 90 days to complete all repairs or risk losing occupancy rights entirely.

The Escrow Solution When Time Runs Out

Here's where many sellers find themselves in a bind: repairs take longer than expected, or contractors aren't available before the scheduled closing date. The solution is repair escrow.

If you cannot complete repairs before closing, you must deposit funds equal to 110-150% of the estimated repair costs into an escrow account managed by the city. This money ensures repairs will be completed after the sale closes, with the new owner receiving the remaining funds once all work is verified complete.

Repair escrow basics you need to nail down at contract time:

- Amount: cities commonly require 110–150% of written contractor estimates; some lenders require higher holdbacks or cap what can be escrowed.

- Who holds the funds: depending on the municipality and lender, the escrow may be held by the city, the title company, or the lender. The holder’s rules control how and when money is released.

- Timeline to complete: typical windows are 30–90 days after closing. Weather or contractor delays may qualify for extensions, but you must request them before the deadline and meet city criteria.

- Release mechanics: funds are released only after the city signs off that every cited item is corrected. Any remainder usually returns to the party who posted the escrow unless your contract says otherwise.

- Missed deadlines: expect additional re-inspection fees, potential fines, a hold on occupancy, and—if city-held—possible draws or forfeiture per ordinance. If lender-held, the bank may extend the hold, require a larger holdback, or refuse release until completion.

- Variability: requirements differ by city and lender. Get written instructions from both parties early and keep them Up To Date throughout the process.

The escrow process protects both parties: buyers know repairs will be completed, and sellers can close on schedule without losing the sale entirely.

Timeline and Enforcement: What Happens If You Miss Deadlines

Cities take point of sale violations seriously, and enforcement varies significantly by jurisdiction. Missing repair deadlines can result in:

- Loss of occupancy permits (making the property legally uninhabitable)

- Inability to close on the sale until violations are resolved

- Additional fines and inspection fees

- Extended escrow requirements with higher financial commitments

- Escrow consequences: when deadlines tied to escrow are missed, cities may levy fines or draw against the escrow; lenders and title companies may extend the holdback or refuse release until completion and proof of city sign-off.

- More re-inspection cycles: each failed or expired re-inspection usually adds new fees and can push timelines further.

Remember, these obligations exist even if you decide not to sell your home after the inspection. The violations don't disappear if you remove your property from the market: they must be addressed regardless. Always verify exact timelines, fees, and extension rules with your city’s building department before you commit to dates in your contract.

Common Point of Sale Violations in Northeast Ohio

After working with hundreds of Northeast Ohio transactions, we've seen these violations appear most frequently:

Electrical Issues: Outdated panels, insufficient GFCI outlets, improper wiring in basements and bathrooms

Basement and Foundation: Moisture problems, inadequate lighting, missing egress windows, concrete crack repairs

Plumbing: Low water pressure, outdated fixtures, drainage issues, missing shut-off valves

Exterior Maintenance: Damaged gutters, loose siding, broken windows, deteriorated concrete walkways

Safety Equipment: Missing or non-functioning smoke detectors, absent carbon monoxide detectors, inadequate stair railings

The total cost for addressing these violations typically ranges from $2,000 to $8,000, though complex electrical or structural issues can push expenses significantly higher.

Strategic Tips for Sellers

Get Ahead of the Game: Request a point of sale inspection before listing your property. This gives you time to address violations without timeline pressure or escrow complications.

Budget Appropriately: Set aside 2-3% of your home's value for potential violation repairs. This prevents last-minute financial stress when violations are discovered.

Choose Contractors Wisely: Work with contractors familiar with municipal requirements. Using inexperienced contractors often leads to failed re-inspections and extended timelines.

Document Everything: Keep detailed records of all repairs and inspections. Cities require verification that work was completed to code standards.

Strategic Tips for Buyers

Factor Violations into Your Offer: If you're aware the property hasn't had recent point of sale inspection, consider that potential violations might delay closing or require escrow arrangements.

Understand Escrow Implications: Money held in city escrow accounts typically doesn't earn interest and may take weeks to release after repair completion.

Verify Completion: If purchasing a property with escrowed violation repairs, ensure you receive documentation proving all work was completed and approved by the city.

Plan for Delays: Point of sale violations commonly extend closing timelines by 2-4 weeks, especially during busy construction seasons when contractors are less available.

Negotiation Strategies That Actually Work

While sellers are legally responsible for violations, buyers can sometimes negotiate assistance through:

- Credit at closing to help offset violation costs

- Extended timelines that allow repairs without escrow requirements

- Shared escrow contributions for extensive violation lists

- Price adjustments that account for known violation costs

Success depends on market conditions, property desirability, and the severity of violations discovered.

Working with the Right Real Estate Team

Navigating point of sale violations requires expertise in local municipal requirements, contractor networks, and timeline management. The wrong approach can cost thousands in additional fees, extended escrow arrangements, or lost sales entirely.

At Milestone Property Group, we've guided hundreds of Northeast Ohio buyers and sellers through complex point of sale situations. Our team understands the specific requirements across local jurisdictions and maintains relationships with contractors experienced in municipal compliance work.

Whether you're selling a property that hasn't been inspected in years or buying a home where violations are discovered, we'll help you navigate the process efficiently and cost-effectively.

Ready to discuss your specific situation? Contact our team today to develop a strategy that protects your interests and keeps your transaction moving forward.

Disclaimer: Point of sale requirements vary significantly by jurisdiction within Northeast Ohio. Always verify specific requirements with your local building department and consult with qualified real estate and legal professionals for guidance specific to your situation. This article provides general information and should not be considered legal or professional advice.

|

or another way